Zoom (ZM) reports earnings today (Monday) after the close.

- ZM options are pricing about a 9% move, or just under $40 in either direction.

- Zoom was lower by -15% on its most recent earnings report and saw moves of +40% and +8% in the two prior.

A full calendar of expected and recent earnings moves can be found on the Options AI Earnings Calendar. Links to Zoom here.

Zoom: Using the Expected Move to Help Create Options Spreads

Using Zoom as an example, we can see how the expected move might be used to help guide strike selection on options spreads, both debit, and credit. We can also see how option spreads can be used to help reduce capital outlay and potentially improve probability of profits (versus buying outright calls or puts).

Zoom Debit Call Spreads

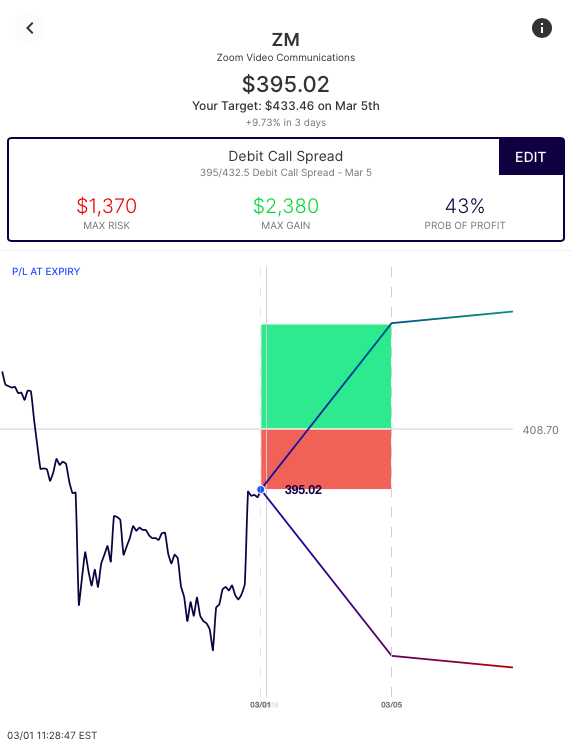

With ZM trading near $395 we can use the 9% expected move to generate spreads, both debit and credit and then compare those to outright calls and puts. Here’s an example of bullish spreads based on the expected move via Options AI:

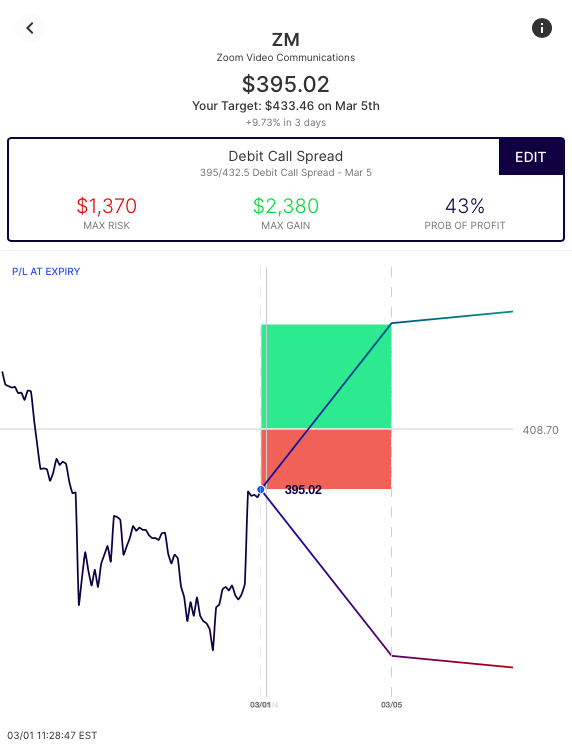

We see two credit spreads, and one debit spread. We’ll focus first on the March 5th 395/432.50 Debit Call Spread. This spread is trading at approximately $14. Here’s how that trade looks on the Options AI chart, with a breakeven near $409:

With this Debit Call Spread a trader is able to position for a move higher at a cost of about $14. The trade needs the stock to be above approx. $409 by Friday’s expiration in order to be profitable.

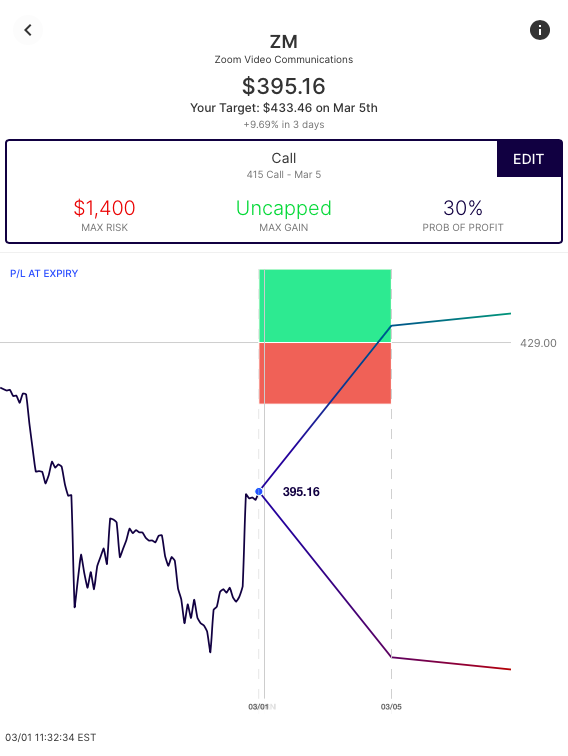

A trader can directly compare the cost of that spread to an out of the money call:

The 425 calls trade at about $14 with a breakeven of $439. So for the same cost of a call, a trader can consider a debit call spread, with a breakeven $30 lower in the stock. Here are those two trades side by side for comparison:

ZM 395/432.5 call spread (March 5th)

ZM 425 call (March 5th)

This is not quite as dramatic as a meme stock like Gamestop where a trader would need to go really far out of the money to find a call trading at the same price as a call spread. Read here for the specifics on GME and other high volatility stocks.

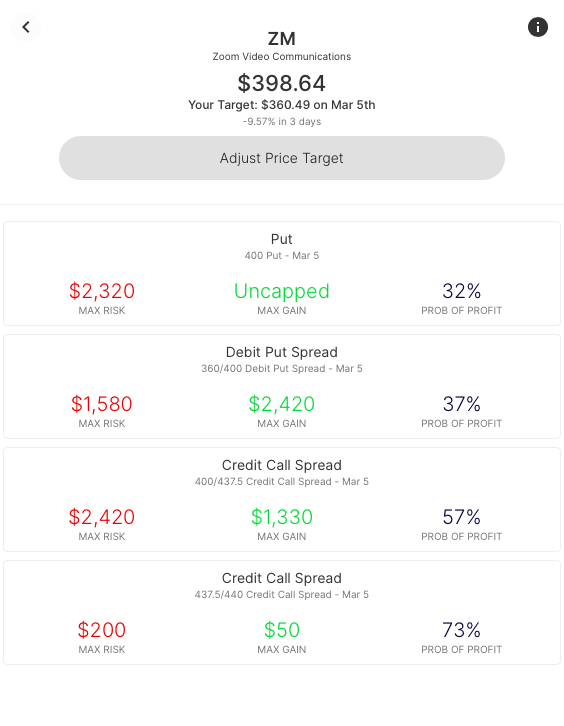

Bearish Debit Spreads – The same process can be applied to Bearish Debit Spreads, with the ZM +400/-360 Debit Put spread trading at about $16:

Directional Credit Spread

Next, we’ll focus on credit spreads. Using Zoom as an example, the expected move can help with strike selection for an out-of-the-money bullish credit put spread. This trade is bullish, but may be best though of as being bullish, by not being bearish:

In this example, the credit spread collects about $70, as long as the stock is above $362.50 on expiry. With this credit spread, more has to be risked ($180) than the potential reward ($70). But, because the trade only needs the stock to be above approx. $362.50 on expiry, it carries a higher probability of profit.

This “bullish by not being bearish” stance is one way traders can express a view in a 230 dollar stock without the higher costs associated of trading options nearer to the current stock price. On a credit spread, the defined ‘risk’, can be thought of similarly to the ‘cost’ one would associate with a long option or a debit spread.

Remember, this should be balanced with an understanding of other risks specific to spreads (such as assignment and execution risk).

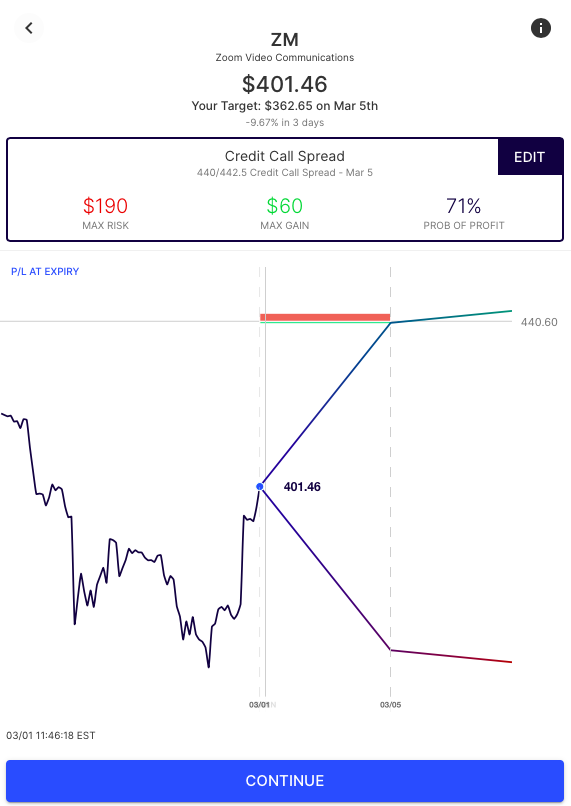

Bearish Credit Call Spread – The same view can be expressed for bearish positioning, in this case with the -440/+442.50 credit call spread:

Zoom Iron Condors – Using the expected move to sell a credit to both the Bulls and the Bears

Finally, let’s consider the scenario where a trader believes that the options market is overpricing the move in both directions and believes that a stock will stay within the expected move. Rather than not bearish” or not bullish like the directional Credit Spreads above, this trade, an Iron Condor, ‘sells the move’ to both the bulls and the bears. An an example, here’s an Iron Condor, selling at a $1 credit:

The Iron condor, which involves simultaneously selling an out-the-money Credit Call Spread and Credit Put Spread seeks to collect the premium (income) received if the stock stays within its expected move.

An Iron Condor is a strategy some traders utilize when they expect implied volatility to go lower. But in this case, with so little time to expiration, the best way to think of this strategy is that if the stock stays within the expected move, it is profitable. If the stock moves beyond the expected move, it is unprofitable.

Note

Please note, any stocks and/or trading strategies referenced are for informational and educational purposes only and should in no way be construed as recommendations. The strategies depicted represent just a few of the many potential ways that options might be used to express any particular view. All prices are approximate at the time of writing. Option spreads involve additional risks that should be fully understood prior to investing.

Learn / Options AI has a couple of free tools, including an earnings calendar with expected moves, as well as education on expected moves and spread trading.