This past week, options prices hit their lowest level since before the pandemic with the VIX dropping below 16 at one point, coinciding with a new all-time high in the SPX. In the days since, the broader market has sold off slightly and the VIX is now back above 20.

For those looking for portfolio hedges or outright directional positioning, options prices are not far off from historical average. There are numerous ways that traders can protect positions, add yield or place outright bearish directional trades if worried about more selling in the markets.

One way to convert current levels of implied volatility into actionable decision-making is by looking at what options are pricing and using that for strike selection. That can then be used to compare both debit and credit trades, depending on the circumstances.

We’ll look at the SPY and compare both credit and debit spreads for those looking for protection, adding yield, or simply those looking for outright bearishness and a follow through on a market sell-off.

SPY Expected Move

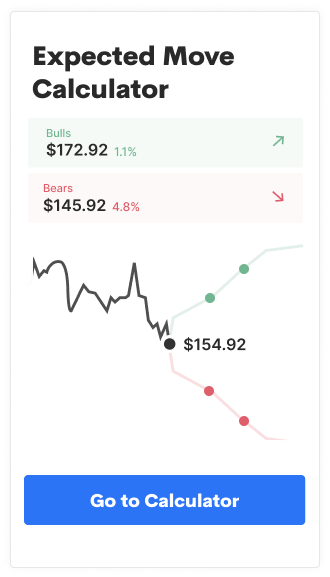

First, a check on the expected move in SPY, via Options AI. The chart below shows an expected move of about 3% out to July 19th. With SPY around 416.50 that corresponds to about 404 on the downside. Close to where most recent sell-off in the market bottomed on May 12th (around 405). So options are pricing a potential move to the downside over the next month roughly equal to the (current) gains over the past month:

.2021-06-18%2008_51_30.gif)

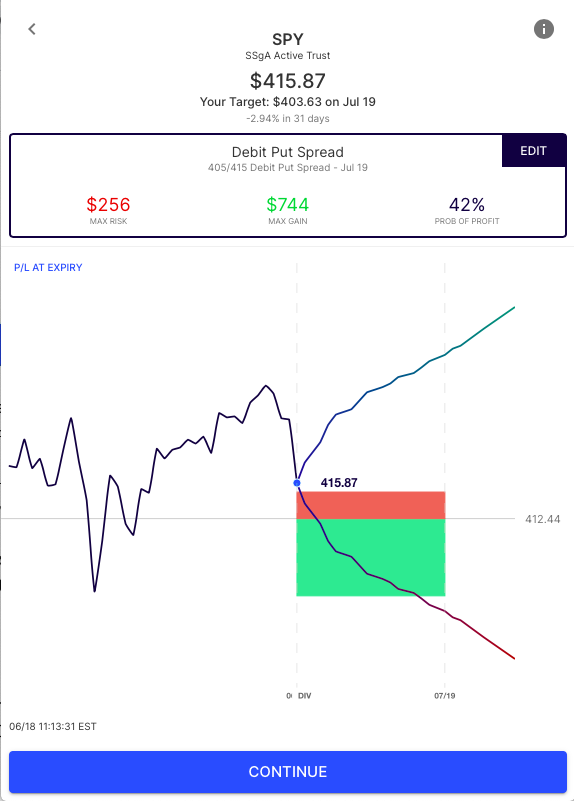

Debit Put Spreads

From a trading perspective, let’s look at some options spreads that use that expected move level. Here’s a debit put spread, generated via Options AI, that buys an at-the-money put and reduces its cost by selling a put at the bearish consensus:

The +415/-405 debit put spread buys an at the money put and sells a put lower, at the expected move. It risks about $250 to make up to $750 if the SPY is at or below $405 on July 19th. It has a roughly 42% probability of profit based on its breakeven around 412.50.

It offers no protection (or gains if outright without stock) below the recent lows of 405. But by selling the 405 put it finances the protection against a move inline with what the option market expects. The 415 put outright would cost a trader $650. Here’s a look at the individual strike prices:

If protection is needed below that level that short put strike can simply be adjusted lower, making the overall trade more costly but allowing for more room below.

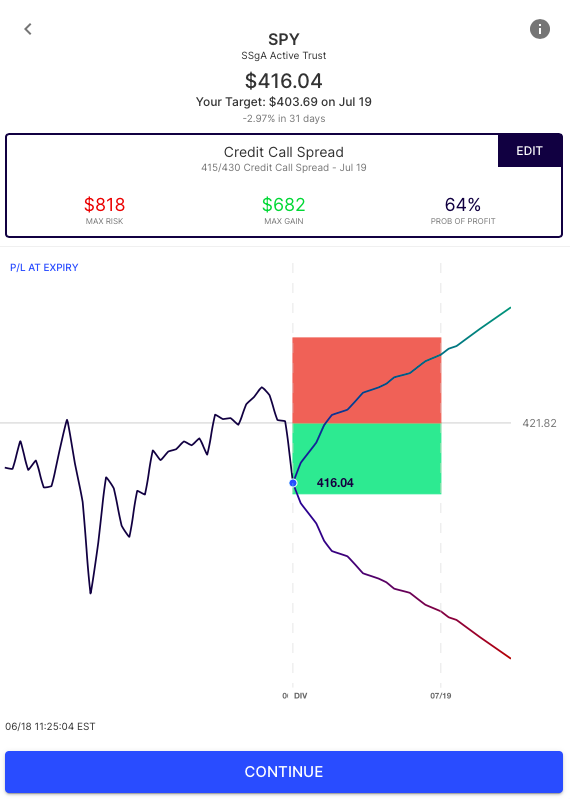

Credit Call Spreads

Another strategy that traders can utilize is selling call spreads. This strategy typically offers less protection in return for an increased probability of breakeven. It can be thought of as a taking a view that is “not bullish”. It looks to gain by the market going down, or by going sideways. And since it can be employed against long stock positions, it can be thought of as somewhat of a hedge.

Here we see the -415/+435 credit call spread. Selling an at-the-money call and defining risk by buying an upside call at the bullish expected move. It risks aboout $820 to make up to $680 with a 64% probability of profit, based on its breakeven around $421.80 in SPY:

This only provides about $680 in “protection” if the market goes lower and risks more than the debit put spread, so it’s therefore more appropriate for those that are not expecting new highs anytime soon. What it does do is take advantage of the slight uptick in volatility over the past few days. If the market were to go lower it would make money on its short deltas, if the market were to go sideways it would make money on decay, and if the market were to rebound slightly it could at least be closed at lower implied volatility, even if booking losses.

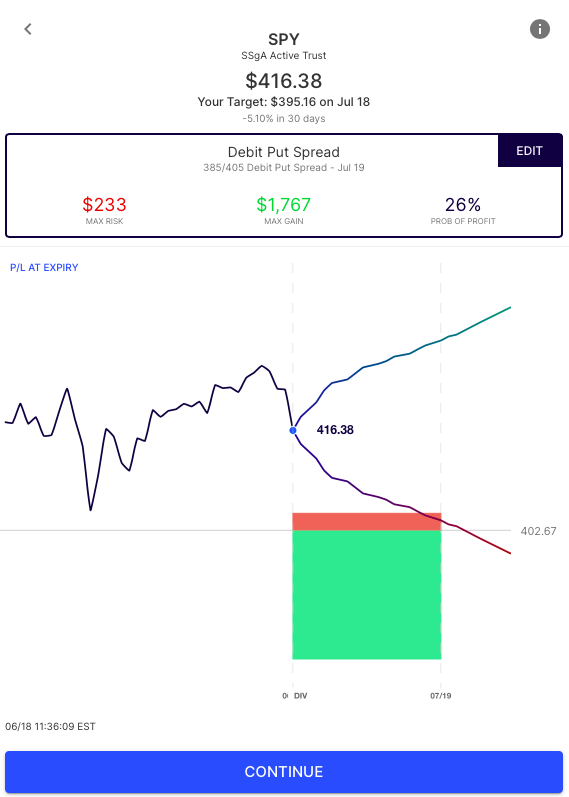

Out of the Money Put Spreads

Another debit spread that traders can employ is “disaster protection”. This is for those that are not worried about a move to recent lows, or what the options market is pricing in, but rather protecting if the options market has it wrong, and a move way below expectations occurs. In this case, a spread can use the expected move as its beginning point, protecting below that move. Here’s a July 19th +405/-385 debit put spread, via Options AI:

The cost/risk of this trade is not far off from the at-the-money debit put spread shown above, but the potential “reward” of the protection is much larger. This is generally not a high probability trade, and a tough way to be right for those looking for outright trades, but for those looking for disaster protection it can make sense, risking just $230 to make up to $1770 and therefore protecting against a large move lower.

Summary

The next move in the market is impossible to know, but options traders have more than one way to express hedges. SPY was used as an example here but the same principles can be used on other broader market ETFs like QQQ and IWM, or even in individual stocks. Additionally, sizing matters. Many traders don’t look to protect the entire value of their underlying, sometimes just a portion. By thinking of these trades in max risk/ max potential gains a comparison can be made to potential gains or losses in the underlying.

Based upon publicly available information derived from option prices at the time of publishing. Intended for informational and educational purposes only and is not any form of recommendation of a particular security, strategy or to open a brokerage account. Options price data and past performance data should not be construed as being indicative of future results and do not guarantee future results or returns. Options involve risk, including exposing investors to potentially significant losses and are therefore not suitable for all investors. Option spreads involve additional risks that should be fully understood prior to investing. Securities trading is offered through Options AI Financial, LLC a registered broker-dealer.

Add comment