Bull Put Spread

BULLISH INCOME STRATEGY, ALSO KNOWN AS A BULL PUT SPREAD

A Credit (Bull) Put Spread is a two-leg options trade where we sell a Put option and simultaneously buy a lower strike Put. The strategy has defined risk and defined reward.

It is commonly used as an income generating strategy by generally bullish investors seeking a probability of profit greater than 50% in return for accepting a higher risk to reward ratio.

It might also be used as an alternative to a Short (Naked) Put by investors who are willing to accept somewhat less premium (income) in return for creating a defined risk position with protection against a sharp move lower in the underlying stock.

Watch the 1 minute overview:

Credit Put Spread (vs Short Put)

To look more closely at the Credit Put Spread and how it might be as used as both a standalone income strategy, as well as a potential alternative to simply selling a Put, we’ll take a hypothetical example using META.

To clarify, we are not suggesting that a Credit Put Spread is always a direct alternative to a Short Put (although there are times when it can be that we discuss below). The Credit Put Spread is often utilized as an income generating strategy where the investor has no intention of owning the underlying stock. The Short Put on the other hand is often used by investors willing to purchase the underlying stock at a level below its current price. With this in mind, the similarities in setup can be useful in helping our understanding of credit spreads.

The Setup

Short Put

In this example, we start by establishing a level at which we believe the stock will find support in a downward move. To inform this decision, we decide to look at the expected move for our timeframe and notice that this also corresponds with a recent low in the stock – around 4.5% lower than the current stock price.

We decide to sell the 157.50 Put at $1.65, collecting $165 in premium. This $165 in income represents our maximum potential gain from the position. If the stock moves down and through the 157.50 strike at expiration we incur the risk of being assigned (forced to buy) the stock at this level. If the stock moves down and through our breakeven level of 155.85 (strike less premium received) then we could incur unlimited potential losses (down to a price of zero in the stock).

Short Put to Credit Put Spread

Now, instead of simply selling the 157.50 Put, we look at simultaneously buying a lower strike Put to reduce our maximum risk in exchange for collecting less premium.

In this example, we are focused on minimizing our maximum risk and therefore look one strike lower, deciding to simultaneously sell the 157.50 Put at $1.65 and buy the 155 Put for $1.10 to open a 157.50/155 Credit Put Spread for a net credit of $0.55 ($1.65 minus $1.10).

Since we are focused on minimizing capital at risk in this example, we create a relatively narrow (one strike width) spread. We could then adjust our overall sizing by increasing the number of contracts traded. However, if we were looking to modify our initial risk to reward ratio, then we might also increase the width of our spread by adjusting our strike levels. Options AI makes finding the right balance of risk, reward, probability of profit straightforward, with the ability to modify profit zones and breakeven levels straight from a chart.

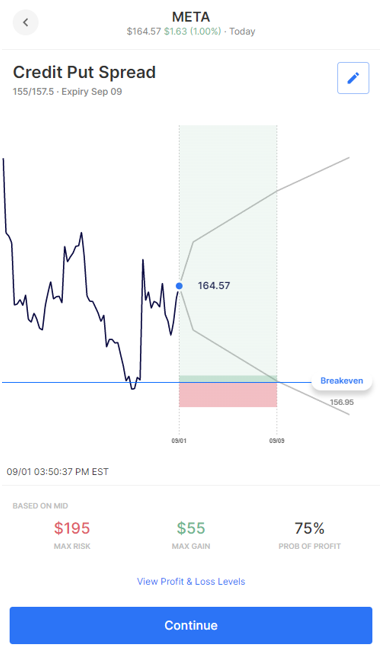

Visual Setup

This visual setup using the Options AI platform shows that, in comparison to a Short Put (which we know has a zone of potential loss down to zero in the stock), the Credit Put Spread has a defined loss (red) zone. In this example, our Max Risk of 1 contract size is $195 (width of our spread less premium received). However, our maximum potential profit has also been reduced and our breakeven level has risen to 156.95 (short strike less premium received).

Perhaps the most noticeable metric (which is typical for both the Short Put and Credit Put Spread) is the relatively high probability of profit. We will look at this in more detail in the summary below.

Summary

In this Credit Put Spread example we have a defined Max Risk of $195. That’s the most that we can lose if the stock closes below our long 155 Put strike at expiration. We will see gains if the stock stays above the breakeven of 156.95 and a Max Gain of $55 if the stock stays above our short 157.50 strike at expiration.

What may become apparent from the visual and associated metrics is why the Credit Put Spread is a favored strategy of bullish investors who prefer higher probability income strategies over lower probability directional strategies (such as buying a Call or Debit Call Spread).

As a net seller of options, we can profit from something not happening rather than needing to be right on direction and magnitude of move. In the case of the Credit Put Spread we create a breakeven below where the stock is currently trading. So, while we are generally bullish we don’t need an outsized move upwards to realize a gain, but simply for the stock to remain above this level at expiration.

Check out our options trading courses to learn concepts like spreads, covered calls, iron condors and more.